- Car loan experts are in a heated debate over the rise of extended loan terms.

- While monthly payments may seem manageable, consumers risk owing more than their vehicle is worth.

- Despite rising car prices and interest rates, some argue that payment-to-income ratios remain stable.

- The long-term affordability and equity implications of extended car loans are under scrutiny.

Eat My Dust The Great Car Loan Debate

Hey, what's up, dudes It's Bart Simpson, your favorite investigative reporter, hot off the press or, well, the internet. I'm diving headfirst into the wild world of car loans, where grown-ups argue about money like Milhouse argues about comic books. So, get this one guy, Sanjiv Yajnik from Capital One Auto, is all chill about rising car debt. He's like, "Everything's coming up Milhouse" because people aren't spending a bigger chunk of their income on cars than before. Even with those sky-high prices, they're somehow making it work. Or are they?

Cowabunga Affordability vs Forever Loans

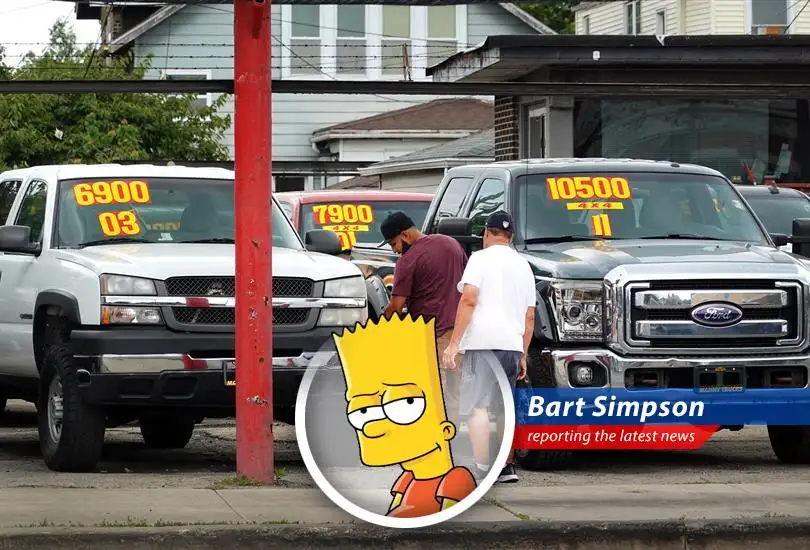

So, how are they doing it, you ask? Easy peasy, lemon squeezy longer loans. But here's where things get dicier than Principal Skinner's dating life. These "forever loans," as some call 'em, stretch out for like, six years or more. Which means you might be paying for that sweet ride long after it's turned into a rusty bucket of bolts. Jessica Caldwell from Edmunds is waving a red flag, saying people end up owing more than their car is worth. Imagine trading in your car and owing like, five grand just to get rid of it. Ay, caramba That sounds like a financial wedgie of epic proportions. For more information on the financial risks, be sure to check out SAVE America Act Sparks Heated Debate on Voting Rights, although that's about voting, car loans are equally important.

Don't Have a Cow The Negative Equity Nightmare

Speaking of owing more than your car's worth, let's talk about negative equity. Edmunds says a whopping 26% of used cars traded in this year had negative equity averaging over five grand. That's like buying a Krusty Burger and finding out it's made of old gym socks. Nobody wants that. And for new cars, it's even worse. Almost all loans with negative equity stretched out for at least six years, with a big chunk going for seven. The average debt carried over was over seven grand. Ouch. That's gonna leave a mark, man.

I Didn't Do It The Blame Game

So, who's to blame for this car loan calamity? Some say it's those pesky rising car prices. Others point the finger at low inventories during the pandemic. But maybe, just maybe, it's those tempting long-term loans that make it seem like you can afford that shiny new ride. But remember, kids, the longer you take to pay it off, the more you'll shell out in interest. It's like buying a Squishee one sip at a time you end up paying way more in the long run.

Excellent A Risky Gamble

Yajnik, however, sees the glass as half full. He argues that people are using their cars to earn money, so it's a worthwhile investment, even with those crazy-long loans. But what happens when your car turns into a lemon? Repairs can cost a fortune, and eventually, you might have to send it to the junkyard in the sky. Then you're stuck with no car and a pile of debt. That's worse than getting detention from Mrs. Krabappel.

Aye Caramba The Bottom Line

So, what's the moral of the story? Car loans can be a real trap if you're not careful. Do your homework, shop around for the best rates, and think long and hard about whether you really need that fancy new car. And remember, kids, don't have a cow, man But do be smart about your money. Or else you might end up living in a box under a bridge like Grandpa Simpson. And nobody wants that.

car loans auto finance consumer debt used car prices longer loans negative equity payment-to-income ratio Edmunds Capital One Auto Sanjiv Yajnik

Comments

From Bart Simpson

Breaking News

All Rights Reserved © 2023

B5049

These long car loans feel like a trap. I'm worried about being underwater.

lolliestancati

I'm sticking with my old car until prices come down. No way am I getting into a long-term loan.