- Nvidia's Q1 earnings report is highly anticipated, with a focus on GPU sales in China and their broader customer base.

- US authorities have approved some Chinese firms to purchase Nvidia's H200 GPU, but Chinese approval and actual deliveries remain uncertain.

- Nvidia faces increasing competition from CPU-focused chipmakers due to evolving AI system architectures.

- Analysts expect Nvidia to beat expectations, but diversifying its customer base and product set is crucial for sustained growth.

The Chinese Enigma: A Market Fraught with Peril and Promise

The game, as they say, is afoot. Nvidia's impending quarterly report is not merely a financial disclosure; it's a high-stakes drama unfolding on the global stage. The central question revolves around the sales of their graphic processing units (GPUs) in China. It appears the American trade authorities have granted approval to approximately ten Chinese entities to acquire Nvidia's second-most formidable H200 GPU chip. A curious development, wouldn't you agree? But, as with all matters of international intrigue, the devil is in the details. Deliveries are yet to be confirmed, and whether these ten firms have secured clearance from Chinese trade authorities remains shrouded in mystery. A trifecta of Chinese internet companies were allegedly permitted to purchase these chips earlier this year, yet the specifics remain elusive. As I always say, "It is a capital mistake to theorize before one has data.", and in this case, the data is as scarce as hen's teeth.

Huang's Gambit: Navigating the Geopolitical Chessboard

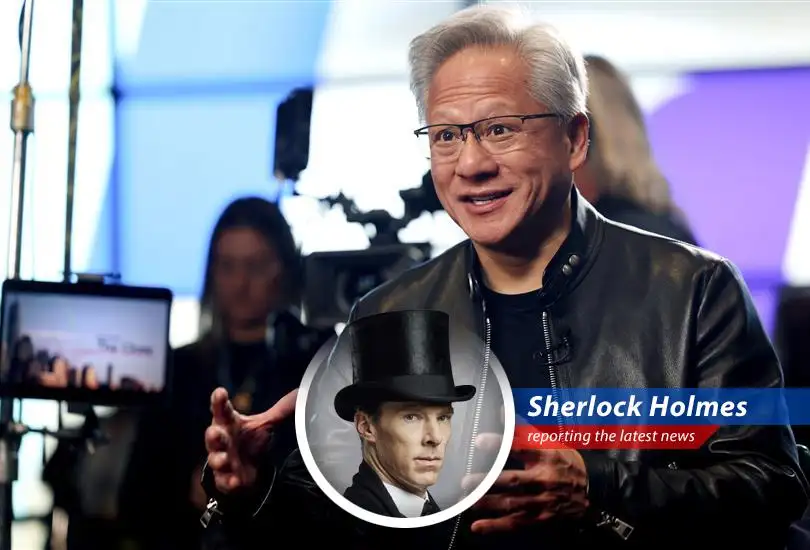

Jensen Huang, the CEO of Nvidia, recently ventured to Beijing, a sojourn coinciding with President Donald Trump's visit earlier this month. Huang conveyed his belief that the Chinese market would eventually reopen to Nvidia. His previous observation that Nvidia's Chinese market share had dwindled to zero certainly adds a layer of piquancy to this situation. "The Chinese government has to decide how much of their local market they want to protect," Huang remarked. A shrewd observation, wouldn't you concur? Trump himself chimed in, noting that China's reluctance to purchase the H200s stemmed from a desire to cultivate their own technological prowess. The intricacies of this timing are of paramount interest to investors and analysts alike. Speaking of high-stakes gambits, consider the potential impact of geopolitical events on the housing market; you might find the insights in this article illuminating: Iran War Sparks Mortgage Rate Surge: Is Homeownership Doomed.

The Analyst's Lens: A Strategic Chess Move or a Fleeting Opportunity?

Kevin Cassidy of Rosenblatt Securities aptly notes that H200 sales into China are more strategic than a matter of pure revenue. The standardization of Chinese AI developers on Nvidia GPUs is a significant consideration. Truist analysts also maintain a watchful eye on sales into China, acknowledging the uncertainty surrounding licenses from Chinese trade authorities. William Stein of Truist posits that sales to China remain a potential upside but stresses that these customers have not yet been awarded import licenses by the Chinese government. The Chinese embassy in Washington cryptically stated that recent discussions between President Xi and President Trump are "pointing the direction and providing safeguards for economic and trade cooperation between the two countries." Intriguing, isn't it? One might say, "Elementary, my dear Watson," but the true elementary part is yet to be seen!

Beyond the Cloud: Diversifying the Customer Base

While the rising tide of AI spending is indeed buoyant for the semiconductor sector, it simultaneously threatens to erode Nvidia's dominance. The increasing disaggregation in AI systems architecture necessitates a diversification of Nvidia's customer base, moving beyond the usual suspects such as Microsoft, Amazon, Alphabet, and Oracle. John Belton of Gabelli Funds raises a crucial point: "Is this company broadening out its customer base? Because that is a big risk." The concentration of Nvidia's business among a mere handful of large companies, which have collectively depleted their free cash flow, poses a significant challenge. The durability of growth within this segment is, to put it mildly, questionable. As I've often said, "Data, data, data! I can't make bricks without clay!" and the data here suggests a need for broader horizons.

CPUs Strike Back: A Shifting Landscape of AI Architecture

AI query-response workloads are becoming increasingly decentralized, resulting in more specialized system designs that demand more CPUs relative to GPUs. Nvidia now finds itself compelled to share the capital expenditure with memory makers, AI networking, and server CPU vendors. HSBC analyst Frank Lee emphasizes the importance of Nvidia demonstrating diversification beyond cloud service providers to sustain its AI GPU momentum. The surge in semiconductors that began in late March, particularly among CPU-focused chipmakers like Intel, AMD, and South Korean manufacturers, underscores this shift. Architecture changes that prioritize coordinated CPU clusters and memory components have allowed these companies to thrive. Nvidia, consequently, missed out on some of the action, and doubts linger regarding its potential gains from ongoing capacity expansion.

High Expectations and Eroding Moats: The Road Ahead

Jay Goldberg of Seaport aptly notes that AMD and INTC have a favorable chance of realizing their potential, while Nvidia remains constrained by high expectations and supply limitations. Updates to frontier AI models necessitating customized architectures could further alter Nvidia's outlook. Mark Lipacis of Evercore ISI suggests that Nvidia's competitive advantage may diminish at the high end, where large customers can justify dedicated teams for alternative solutions like AMD, TPU, Trainium, Cerebras, and internal ASICs. Ulrike Hoffman-Burchardi of UBS highlights the consensus estimate for Nvidia, projecting an 80% year-over-year increase in revenues and a 120% annual growth in EPS. Investors anticipate that Nvidia will not only meet but exceed expectations, offering guidance that surpasses analysts' forecasts. But as always, I believe that "There is nothing more deceptive than an obvious fact."

Comments

From Sherlock Holmes

Breaking News

All Rights Reserved © 2023

Nvision

The increasing power of CPUs is a real threat to GPU dominance.

redeyemist

The China situation is so complex. It's hard to predict what will happen.